What is an SBA 504 loan?

The SBA 504 Loan Program assists small businesses in receiving the opportunity of financing their expansion projects with attractive rates and terms. The financing can be used for the purchase and/or development of land and building for business purposes. The 504 program offers fixed rates for capital expenditures with up to ninety percent financing; the SBA portion can finance up to forty percent of a project's fixed assets.

What can an SBA 504 Loan be used for?

SBA 504 loans can be used for the purchase or construction of existing buildings or land |

SBA 504 loans can be used for the improvement/modernization of land, streets, parking lots and landscaping |

SBA 504 loans can be used for the purchase or construction of new facilities |

SBA 504 loans can be used for the purchase or construction of long-term machinery and equipment |

SBA 504 Loan vs. SBA 7(A) Loan

Value |

SBA 504 LOAN |

SBA 7(A) LOAN |

Loan Size |

Minimum - $100,000 Maximum - $20 million + |

Minimum - $50,000 Maximum - $5 million |

Interest Rate |

Fixed |

Mostly variable; some fixed options available |

Term |

25 years |

Up to 25 years - real estate Up to 10 years - business acquisition and equipment 5 to 7 years - working capital weighted average for mixed requests |

Down Payment |

10% borrower * |

Minimum 10% borrower (often more) |

Business Size |

Business net worth of $20MM or less |

Determined by Industry type |

Loan Structure |

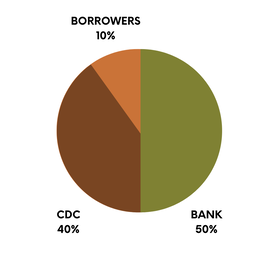

50% bank loan 40% CDC/SBA loan 10% borrower down payment |

Structure negotiable - depending on risk 10% minimum down payment from borrower |

Use of Proceeds |

Purchase of existing building Land acquisition and ground-up construction Expansion of existing building Building Improvements Purchase equipment |

Start, purchase or expand a business Purchase or construct real estate Refinance existing business debt Buy equipment Working capital Leasehold Improvements Purchase Inventory |

Program Requirements |

51% owner occupied for existing businesses 60% owner occupied for new construction Equipment: minimum 10-year economic life |

51% owner occupied for existing businesses 60% owner occupied for new construction All assets financed must be used for the direct benefit of the business |

Collateral |

Generally, project assets being financed are sufficient collateral Personal guarantees of principal owners of 20% or more ownership |

Assets financed by loan proceeds Generally, pledge of personal residence Personal guarantees of principal owners of 20% or more ownership |

Fees |

Fees are financed in the 504 loan Fees for the 50% bank loan Servicing fee plus a legal review fee |

Fees can be financed in the 7a loan Fees vary with the size of loan Additional .25% charged on any loan portion above $1 million |

The SBA 504 loan consists of a first mortgage, for 50 percent of the total project cost, from a third-party lender (local bank).

The SBA 504 loan will be a second mortgage, provided by So Cal CDC, financing up to 40 percent of total project costs.

The remaining 10 percent will be provided by the small business owner as a down payment for the total project costs.

SBA 504 Loan Eligibility

Small businesses interested in purchasing real estate and/or equipment may qualify for the SBA 504 Loan Program.

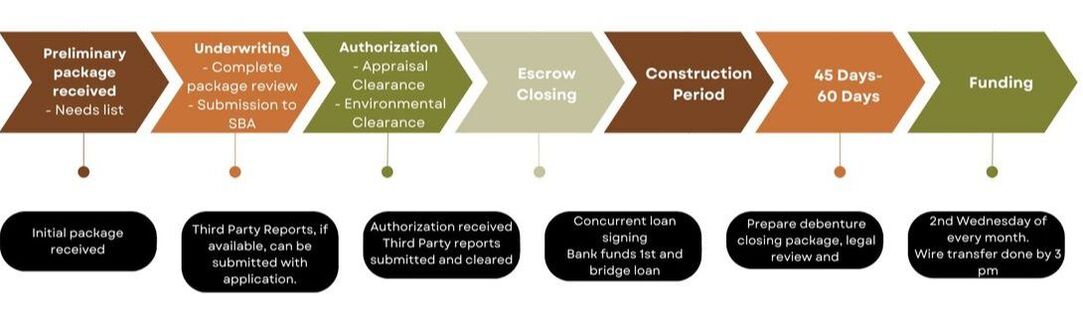

SBA 504 Loan Process